Facebook

Facebook

Twitter

Twitter

LINE

LINE

Scope of house tax:

The house tax shall be levied on all houses attached to land and on such other buildings, which enhance the utility value of said houses. The house includes not only the normal houses but also different types of special buildings that are intended for residential, work, and business purposes, such as loft buildings, various forms of warehouses, fuel tanks, and gas stations.

Taxpayer:

1. House owner. 2. Where a right of Dien exists, the house tax shall be collected from the Dien holder. 3. Where a house is jointly owned by more than one person, the house tax shall be collected from the joint owners who shall designate one person to pay the tax on their behalf, otherwise the present occupant or user shall pay the tax on behalf of the joint owners. 4. In case a house is a trust property and the trust is in force, the taxpayer of its house tax shall be the trustee. In case there are 2 or more trustees, the provision on joint ownership shall apply. 5. In case the whereabouts of the owner or Dien holder of the house referred to in the preceding paragraph is unknown or if he is not domiciled in the locality where the house is located, the house tax shall be paid by the manager or present occupant of the house. In case the house is rented, the house tax shall be paid by the tenant and deducted from the rent payable to the owner. For houses that have never had ownership registered and the whereabouts of the owner is unknown, the house tax due shall be collected from the builder indicated in the use license; in case no use license has been issued, from the builder indicated in the construction license; in case no construction license has been issued, from the current occupant or manager.

House tax calculation:

Standard house price x size (acreage) x (1-an applicable depreciation rate x the years of depreciation) x an adjustment rate based on the level/class of street or road x an applicable tax rate = payable house tax.

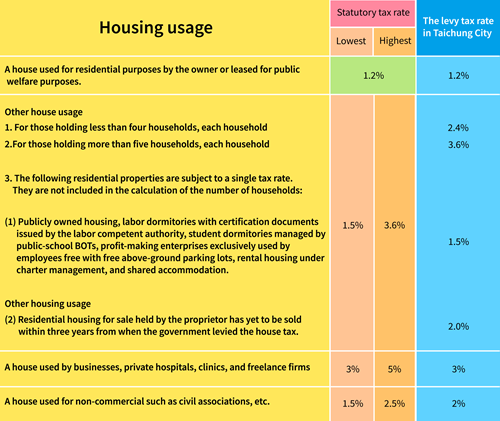

Tax rate: